ESKOM case study: This is how Ramaphosa is assisting the White Monopoly Capitalists to loot and destroy the SoEs

By Lebogang Hovenga

Sometime in 2016 Thuli Madonsela released her report into state capture, heavily implicating Brian Molefe in corruption and collusion with the Guptas...

If you bring solutions to the SoEs you are in trouble: Brian Molefe, whose solutions for Eskom saw him being quickly pushed out

The report seems to have caught Molefe off-guard. He broke down. He cried. Some days later, he resigned. Something that was already in the public domain caused me to empathize with Molefe. Politics is a small world, rumours spread, people talk, they gossip.

About a month or two before the report, a friend who works for Eskom bitterly complained about what seemed to be draconian security measures around Molefe, then a new CEO. It all sounded like resentment to me, so I dismissed it. But fact often jump at you in stranger ways than fiction.

Molefe is a reasonable public figure who lives in the upmarket estate of Cornwall hill. He had lived there long before he joined Eskom, while he was CEO of Transnet.

Again, human beings make innocent observations. Suddenly Molefe had two armed-guards stationed outside his house. So you did not need an intelligence report to notice that security around him was beefing-up fast.

This is when the rumours started in ANC circles that his house was robbed. His family was allegedly held at gun-point.

Saucy rumours are agile and tall on their feet. It was also said that his driver had noticed they were being followed. There might have been a hijacking attempt as well. Now I cannot confirm it for you but that is what was in the public domain. How did I know that he had two guards stationed outside his house? By nothing but sheer coincidence.

As Molefe was being lampooned, I said to a colleague who lives in Irene: “Cut the man some slack, he has just been appointed CEO at Eskom, he has just re-married, he is being followed, robbed , now Thuli. If I were him, I would also cry buckets and resign.”

I kid you not, my colleague responded: “Oh is that why Brian suddenly has heavily armed guards outside his house?”

So look man, I don’t need to be a spy to know this. What does this have to do with Glencore? Indulge me, I will give you your 80%.

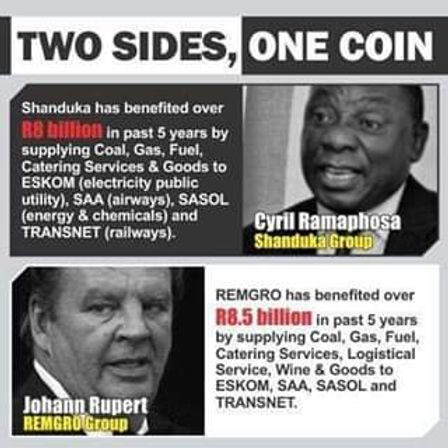

In 2012, Cyril Ramaphosa was elected Deputy President of the ANC. At the time I was one of Kgalema Motlanthe’s speechwriters. Naturally I became curious about the man who would one day become my boss. I knew then that his company Shanduka Resources was in joint-venture with mining giant Glencore, trading as Optimum Coal. And so in a conversation with a Glencore executive, I asked what it is like to work with Ramaphosa. The answer was crude and racist.

The same answer was repeated some time later in a book: Murder at Small Koppie by Greg Marinovich. Marinovich accused Ramaphosa of fronting for Glencore. He claims that an unnamed Glencore executive told his business partners: “I don’t want to be crude, but we made him (Ramaphosa).”

So look, I don’t need to be a spy to know that Glencore Executives— it may be just one—have a habit of thinking black people are puppets. Now those who listened attentively to Molefe's testimony would have noticed that he kept emphasizing that— this Papa Action thing— “people could not believe that anybody could ever speak to Glencore like that.”

Now I don’t know if this, what is in the public domain, makes 80%. However, I am willing to bet my bottom dollar that those Glencore people had no respect for Molefe. If they could be so crude and racist about the Deputy President, I think undermining an Eskom CEO was par for the course.

But if there is a black man who carries himself with the confidence of a mediocre whiteman, it is that Molefe fellow. So I think part of the problem was a clash of egos.

Something else caught my attention in Molefe’s evidence, which I also had knowledge of by sheer coincidence. He kept emphasizing the need to review all apartheid era Eskom contracts if we really want to get to the bottom of state capture.

Now I know a little bit about these contracts. There are many dots to join to get to 80%, but I will take you there.

In 2007, I worked for the Sales and Marketing division of Transnet TFR. What we were learning from those apartheid era contracts is that certain mining companies were benefiting from SoE’s in ways they were not morally entitled to. For example, a multinational company would start a mine kilometres from a main railway line. Their contract would read that the mining company is only responsible for capital expenditure on loading equipment and rail lines within its premises.

That meant Transnet would have to buy land, pay for infrastructure and the maintenance of lines in-between. This is not necessarily a bad thing if Transnet priced appropriately.

But what would happen is that Transnet would bill per ton or number of wagons loaded. Now, if workers went on strike at the mine, or there was insufficient production, Transnet would still have to pay electricity and other maintenance costs on the line.

But a train is not a jalopy. If it is not loaded, it has to stand. It cannot be used for other purposes. This is what economists call opportunity costs. If something else comes up, the train has to be recalled. It is still an empty train, there is no price per ton, and somebody has to pay for it. In theory this is inefficient and translates to high capital costs. You literally have to buy a larger number of wagons and locomotives than is necessary.

When the mine closes, Transnet is stuck with land and a useless line. To prevent further maintenance costs, Transnet will then have to lift the line and so on. This is amongst some of the reasons why you have a healthy looking Transnet balance sheet, but there is no concomitant cash or income generation.

Now some people will argue that it is the duty of the state or SoEs to provide economic infrastructure. Correct. Only, trains are not infrastructure. The rest of the world, they operate on the-user-pays principle. Just as it is the duty of the state to build roads to enable me to drive to work, and generate an income, it is not the duty of the state to buy me a car and maintain it.

All things equal, the business of Transnet is to avail trains and railways, not to carry the operations costs of large mines. So we were being robbed silly. What is more painful about this is that supper profits were made and taken offshore.

Moreover, black and SMMEs were required to hire trucks to transport their produce to the mainline and we would still wonder why there is no competition against White Monopoly Capital.

Again, what does this have to do with ESKOM?

When Brian Molefe joined Transnet, it was in the process of trying to renegotiate these contracts and apply the-user-pays principle. So whether a train was loaded or not, if the train arrived on time it was to be paid for and loaded to leave on time. Time is money.

Glencore is one of the big 5 coal producers that collectively controls 85% of coal mining operations in SA. When Transnet was pleading hardship and bleeding money, Glencore refused to sign the new deal. It used all delay tactics it could master. This is in an environment where the tax-payers were carrying the cost and providing painful state guarantees to Transnet.

I suppose at the time, Glencore, could have never imagined that Molefe would one day become the CEO of Eskom. Neither did they foresee that they would themselves fall on hard times. So forgive me for asking why did we expect Brian to have treated them with courtesy?

This does not make what Brian did right, it only provides a context.

What was really at issue is Glencore’s sense of entitlement and an insidious culture of looting public coffers for profit.

It actually gets worse than bad. (We are still operating within the 80% publicly available intelligence.)

So what is available? The internet and books. One example is titled Blackout—The Eskom Crisis by James-Brent Styan.

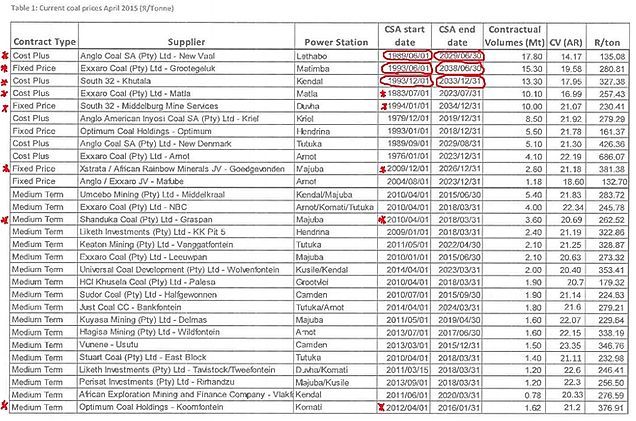

South Africa is a very coal rich country. It is estimated that we have coal reserves that can supply both our electricity needs and exports for the next 200 years. You will recall that the Apartheid government had a strategy of self-sufficiency in the wake of international sanctions. They devised three main uses for coal. The high grade coal would be for export and for SASOL to extract fuel. The lower grades would be used for generating electricity. Eskom power stations were therefore designed for this low grade coal. Coal mines also modelled their operations according to this structure.

So if you wanted a coal mining operation in South Africa, Eskom would incentivise me by building a power station next to your mine. They would carry some of the start-up costs thus to pre-pay you for coal. The rest would be paid on delivery. The average cost in today’s prices works out to between R1000-R1500 per ton. To recoup this cost you had to guarantee supply over most of the power station’s useful life. So you would enter these ever-green contracts some for 40 years at fixed prices. If the mine fell on hard times, you could plead hardship and Eskom would assist you to recover.

There was some method in this madness. You cannot mine and export quality coal without producing the lower grade needed by Eskom. Your profits would mostly come from exporting high-quality coal and sending the rejects to Eskom. There was however a downside to this lower quality coal. If you sent the lowest quality than the standards set, heavy levels of ash and residue build up and cause breakages.

Now thieves are thieves. These companies would mix the coal that you and I should braai with together with Eskom quality coal. So Eskom created a dumping penalty system. For reasons still unknown.

Glecore-Shanduka-Optimum’s penalty fees piled-up to a staggering R2 billion by 2015. So they delivered bad coal, they were paid in full for it and nobody bothered to deduct the fines. But thieves are thieves you see, they won’t remind you if you can’t run your administration properly.

Now I can explain where the Guptas come in.

About 80% of all these long-term contracts were coming to an end in 2018. One for Exxaro was ending in Dec 2015.

Another of these contracts was originally signed with BHP Billiton – Optimum Coal Holdings, which supplies the Hendrina Power Station.

In 2008 BHP sold Optimum to a BEE consortium led by Eliphus Monkoe and about 13 others. This was a strange transaction. BHP sold a mine to black people, and guaranteed to buy only the export quality coal from them. I don’t know about you, but this is the most generous white capital has ever been to a black man.

I cannot for the life of me tell you why these fellows bought this mine in the first place. I think they were sold a lemon. Within a period of two years, in 2010, they listed Optimum on the JSE and began selling their shares like hotcakes. It tells you something, they were losing money fast. On paper the mine looked promising. It had a guaranteed buyer, BHP Billiton, for its export coal and a long-life contract with Eskom. But actually getting the coal out of the ground was another story. Nonetheless the company was a hit with the markets. On day 1 the market cap had grown by more than R2 billion.

But why do companies list on the stock-exchange? To raise money for expansion and growth, right?

Well not quite. Here was this black consortium with the brightest future, but its original directors were selling as if they were running away. One director allegedly sold all his shares within a matter of months. Me I don’t know, but I was taught in undergraduate economics, that there is something horribly wrong with the directors of a company selling their shares in that fashion. One word— Enron!

So in 2012, less than 2 years after listing, Glencore and Shanduka Resources bought Optimum at more than it was worth and delisted. Eskom approved the sale on condition that in the event of the mine failing, Glencore, the global giant, would be liable for liquidation guarantees.

Remember, Eskom had invested and paid upfront for the coal. Because of these rights; Eskom had to approve any sale or transfer of Optimum until it recouped its fair share.

But why did Glencore and Shanduka buy Optimum if it was bleeding money? Well, I think it was a brilliant business strategy. They were not buying current Optimum operations, they were buying future operations. Eskom had just committed to a new build programme which would give preferential treatment to BBBEE companies. Of all the big 5, Exxaro was the only one with full BEE credentials, it was 51% black-owned. Not only that, 2018 was 5 years around the corner.

Put differently, if Glencore/Shanduka wanted a new coal mine in time for 2018, it would have to not only secure new mining rights but also to carry the original capital costs. A smart business man lets other people pay for the infrastructure and milks the cream off the top.

So for Glencore having Shanduka Resources as a partner helped kill three birds with one stone. Firstly, it was buying existing mining rights under Optimum for both export and Eskom supply. Secondly, Exxaro was no longer a fully black-owned company. Its black share-holding had dropped from 51% to 30%. Its contract was due to expire and would have a lot of explaining to do to win another contract. Thirdly, from 2018; Eskom was more likely to negotiate and prepay for new mines if they had good BEE credentials.

So far so good, this is all public information and everything was perfectly legal and above board.

By 2015 Optimum owed R2.7 billion to banks and some R128 million to Shanduka Resources. The mine was experiencing a number of operational challenges. According to reports, for 3 months it was producing close to 88% percent of Eskom quality coal and not exporting much. Export is where the profits were supposed to come from. But whatever the difficulties it had to deliver on its contract with Eskom, it was only receiving R150 per ton but production costs were estimated to be R179 per ton, which it could not sustain without exporting. Therefore a reasonable man, Thuli Madonsela included, might very well have said: “Optimum had fallen on hard times, there is a hardship clause, and it is entitled to an increase.”

But not so fast. There is some nuance. Optimum was the author of its own misfortune. I suspect, if Madonsela had provided Molefe an opportunity to explain, she could have found 3 things.

First, Glencore-Shanduka-Optimum was refusing to sign the train contract with Transnet thus refusing to pay a fair user-pays price, in the process shifting the burden to the taxpayer. So it may have left Transnet under Molefe no choice but to delay its exports.

Secondly, during the 15-year period of the contract, when coal exports were booming, Optimum had asked Eskom on two different occasions to allow them to focus on exporting; in return they lowered their price to R150 per ton. Given this background, it may not have been entirely true that R150 was an unfair price.

Thirdly, while it remains true that Glencore-Shanduka-Optimum was having a tough time spending R179 per ton; this was not a cost change that Eskom was supposed to carry. Glencore is a global mining company, it has no right simply because things have gone wrong in South Africa to shift the blame onto Eskom. It was not losing global profits, it was losing South African profits.

It also seems to me that most of the operational difficulties were on the export side of operations. When you mine coal you may have difficulty reaching the seam with export quality coal. You may also have challenges with our separation or coal washing operations. But in the process of trying to get to the export grade you still produce Eskom quality coal— which was already paid for. You must still deliver.

But Karma is a b*tch. When Molefe was moved from Transnet to Eskom he knew of Glencore's antics. He knew that the operational difficulties that got them pleading hardship were not Eskom related. The hardship claimed for export was none of Eskom’s business.

In fact I think Glencore was crude. They were only pleading hardship for Hendrina, not all its coal operations. I think this may have been dishonest. What is claimed today is that the global market rate was about R570 per ton. They were only asking for an increase to R400. But why did they not ask for the R179 per ton it was costing them? Why was Eskom supposed to pay more or market rate when it had already spent R1000 or so in advance?

Former Eskom senior executives, including the CEO of Tubular Construction (second from left) accused of defrauding the parastatal for more than R700 million: Mangope France Hlakudi, Antonio Jose Da Costa Trindade, Abram Abel Masango and Maphoko Hudson Kgomoeswana

Now you will be told that ESKOM was also paying Anglo and Exxaro about R1000 per ton. Yes R1000. So to export quality is around R570, we pay R1000 for rejects? Injani le Kapital (what kind of capital is this)? Why does this entitle Glencore to an increase at our expense?

You see thieves are thieves. This is another problem with what is called cost-plus contracts. They would claim that the price of producing coal is R570 for export grade. But they then add about R150 for transport and another R300 for labour. That’s how they justified the prices around R1000. But if the export market buys higher quality at R570, why is Eskom paying R1000 for a cheaper by-product? Looting. This so called cost-plus method allows mines to shift their labour costs to Eskom.

Now this Molefe fellow was a new broom, he was sweeping clean. He told them all that come 2018 the looting is over.

Now this is where the Gupta brothers and Brian Molefe start skating on thin ice. When Molefe arrived at Eskom he wanted to do what was started at Transnet. 80% of all these nonsensical contracts were coming to an end and he gave all the giants notice that Eskom may not renew. Hence “Papa Action.”

When Molefe was transferred he arrived at Glencore-Shanduka-Optimum already in negotiations with Eskom. It was during load-shedding, downgrades and liquidity problems. Eskom was itself in hardship.

Glencore was asking for a helping hand from a tax-payer who was already struggling. Molefe refused. Glencore, with full bravado and the confidence of a mediocre Whiteman threatened to stop supply—during load shedding! So he called their bluff. Unfortunately they had met their match.

According to Eskom’s stockpiling policy each station must have 28 days of coal readily available. So stopping supply at Hendrina would not have an immediate effect on load-shedding. So in the process of trying to force Glencore to supply, Molefe “accidently” came across the R2 billion fine that was always due but never paid.

This is what Glencore-Shanduka-Optimum claims forced them into business rescue. Molefe claims that they only decided to apply for business rescue because that was the only way they could lawfully stop supply. In toto, they could still mine Eskom quality, so no court would have allowed them to stop supply without good cause.

The sequencing is complicated but this is what happened in a nutshell.

What did this mean for Glencore? It was now liable to all Optimum's debtors in terms of the guarantees it signed when it bought Optimum with Shanduka Resources. This was some R2.7 billion to commercial banks and a R128 million loan from Shanduka.

According to Molefe’s testimony it was during this stand-off that Eskom discovered 9 small coal producers who could sell coal to Hendrina at R400 per ton.

Now this is where the alleged hijacking happens. I believe the (apartheid) media has covered this aspect in sufficient detail, I disagree with very little in their version. I am only trying to put the version that was not explained properly to the Public Protector.

Now at the time Glencore-Shanduka-Optimum was caught in this fight; Pembani was in the process of buying out the Deputy President Cyril Ramaphosa out of Shanduka. Optimum Coal was part of that deal.

This complicated what Pembani had to pay for the Shanduka sale. What would the due diligence cost of Optimum be given the loan and possible goodwill changes?

So in another stroke of genius Pembani put in an offer to buy its own Optimum mine. This was like buying Optimum without assuming responsibility for what Glencore owed to banks. Possibly it could also later write-off its own R128 million loan to improve its balance sheet.

Remember, part of the strategy was to get to 2018. They were also planning to buy Exxaro thus to create the biggest black coal company in time for 2018. I think they would also score on what they paid Ramaphosa because his hands were now tied. He was now Deputy President. Glencore, on the other hand, was stuck with the guarantees for the debts with banks. So for Pembani, buying its own subsidiary was a bloody good deal.

But Eskom had concurrence rights and a R2 billion fine. So when Pembani made an offer it was conditional. They were only making the offer on condition that Eskom would drop the fine and sign a new contract to increase the price from R150 per ton.

According to the evidence of the business rescue practitioners, Pembani offered to meet and negotiate with Eskom directly. I guess they were hoping Pembani would speak some sense into Molefe. Molefe also corroborated this in his own testimony.

But this posed an ethical problem. Was this an arm’s length transaction? According to Molefe’s version what Pembani was asking him to do was problematic. If he was refusing to drop the fine for its subsidiary, why drop it for Pembani? The only reason Glencore-Shanduka-Optimum needed business rescue was because of the fine and refusal to up the price. Why would he then do it for Pembani?

As he explained, people would say he directly enriched Pembani to the tune of R2 billion. And indeed it was a self-fulfilling prophecy. Energy analyst Ted Blom was already accusing DP Ramaphosa of improperly benefiting from Eskom. But Ramaphosa has responded comprehensively to this, he was out of Shanduka negotiations by 2014.

So I think part of the problem is that the Public Protector treated Pembani as an arm’s length transaction. She may have not taken full account of the fact that Pembani may have been conflicted or trying to avoid painful loan repayments. Now this is where the Guptas allegedly come in with an offer that under cuts Pembani. It is alleged that the Guptas did not have the money to pay upfront.

According to Molefe, when Pembani heard of the offer from the Guptas, it wrote to Eskom to say it had first option to buy. They were claiming that the mine could not be sold to anyone else under different conditions. This was a reasonable and fair expectation. But this is not cut and dry, nobody said the mine was being sold to the Guptas without the fine. Nor did the Guptas ask for the price to increase from R150 per ton. Though I do think they also had 2018 in mind.

When White Monopoly Capitalists and their Clever Blacks want to steal from the people, they find scapegoats first. The scapegoats in the case of Eskom became the Gupta brothers

But did the Public Protector fully balance all the conflicts of interests? Did she properly take into account that whatever Pembani and Glencore stood to lose, it was going to be transferred to the tax payer? Surely a price increase causes high electricity costs, lower cash and affects the bottom line. Why was Glencore and Phembani more entitled than us? Were we supposed to give ESKOM more guarantees to save Glencore?

So from this 80% of freely available information, I have formulated the view that the PP may have acted in haste.

But that does not mean she was wrong to ask questions on how the Guptas made an offer that was just right and why Eskom gave them the R600 odd million they were short of.

Pembani in this sense was a jilted lover, its submissions had to be treated with caution.

But I hold no brief for Molefe or the Guptas. I am really interested in ensuring that we are never robbed again. I do not for a minute believe Molefe is innocent of all wrong doing, nor do I believe the Public Protector was deliberately targeting him. I think she was caught between a battle of thieves.

In 2018 Eskom needs to sign new contracts. Now we know that small-scale miners can sell at R400 per ton. The Big guys are getting around R1000 a ton. On top of that Eskom either pays upfront for the capital costs or allows the cost-plus looting.

So comrades we can sacrifice Molefe and the Guptas, but we did not send them to join these thieves in the name of fighting against WMC.

Remember, always the words of Amilca Cabral:

“Every responsible member must have the courage of his responsibilities, exacting from others a proper respect for his work and properly respecting the work of others. Hide nothing from the masses of our people. Expose lies whenever they are told. Mask no difficulties, mistakes and failures. Claim no easy victories and tell no lies!

But hush child, zizojik’ izinto.

Ningalali. Nizothengiswa Ngooyihlo.